| 1929, 1973, 1987 and 2000…Why it’s NOT Different This Time |

Tuesday, 27 June 2023 — Gold Coast  | | By Vern Gowdie | | Editor, The Daily Reckoning Australia |

|

[7 min read] | Quick summary: Friendly warning…today’s The Daily Reckoning Australia is long on charts and short on text. These pictures paint more than a thousand words. However, there’s only ONE message from today’s issue and that is…history repeats and now is the time to exercise extreme caution… |

|

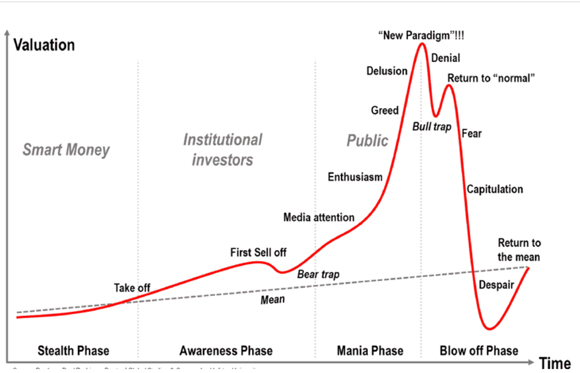

Dear Reader, Friendly warning…today’s The Daily Reckoning Australia is long on charts and short on text. These pictures paint more than a thousand words. However, there’s only ONE message from today’s issue and that is…history repeats and now is the time to exercise extreme caution. In 2006, while the US Housing Bubble was in full inflating mode, Dr Jean-Paul Rodrigue studied bubbles and manias past to formulate this all-too-repeatable pattern of human behaviour. In a detached state of mind, we can rub our chins, nod our heads and think ‘yes, this represents a fair and rational assessment of man’s evolving emotional states’. Yet, when we’re in the middle of it all and markets are playing mind games, it’s not easy to remain so composed. Patterns get repeated — time and time again — because, at our core, we are emotional beings. Amidst the racket of fear and greed, voices of reason are invariably drowned out. There is much whoopin’ and a hollerin’ over a new bull market on Wall Street. Yes, in technical terms, the S&P 500 Index does meet the 20% recovery definition of a ‘new’ bull market. But, as I showed in last week’s issue of The Gowdie Advisory, there were no less than four —and almost five — so-called ‘new bull markets’ in the Dow’s near 90% plunge between 1929 and 1932. Wall Street fortunes rest on one skinny pillar The reality is, there’s genuine bull markets and there are fake bull markets. The latter are ones where only a handful of stocks push the headline indices higher. As of 20 June 2023, the year-to-date (YTD) performance of the S&P 500 Index was 15.24%. However, this performance has been entirely due to the Magnificent Seven. The ‘Top Seven Holdings’ (which account for around 28% of the S&P 500) have shot the lights out. Without the performance of these seven stocks, the remaining 493 stocks have turned in a performance of NEGATIVE 3%. The broader market being supported by ‘one, very skinny pillar’ of support, is not a new phenomenon. Thanks to human nature, there is market precedent. According to Kevin Malone of Greenrock Research, ‘… in 1999, it was the top six stocks. You may remember that this was followed by a stock market that declined for the following three years…’ We saw the same thing 50 years ago The early 1970s version of The Magnificent Seven, was called The Nifty Fifty. As reported by USA Today (emphasis added): ‘The Nifty Fifty captivated investors for the better part of a decade prior to its demise in 1973, but not before reviving the high-risk investing that had been out of vogue since the Crash of ‘29. ‘That optimism was visible in a key measure of the stocks’ value: the price-to-earnings ratio or P/E — the price-per-share divided by the company’s annual earnings-per-share. By 1972 when the S&P 500 Index’s P/E stood at a then lofty 19, the Nifty Fifty’s average P/E was more than twice that at 42. Among the most inflated were Polaroid with a P/E of 91; McDonald’s, 86; Walt Disney, 82; and Avon Products, 65. ‘Along came the stock market collapse of 1973–74, where the Dow Jones Industrial Average fell 45% in just two years.’ While the broader index fell 45%, this is what happened to some of the higher profile ‘Nifty Fifty’…they suffered a greater level of loss… The fate of The Nifty Fifty is proof of ‘the higher you fly, the harder you fall’. And, 27 years later, it happened again The pattern of infatuation with a handful of market darlings comes more clearly into focus with this next chart…‘Top 10 Stocks by Market Cap of S&P 500’. It happened in 1973, and we’ve shown how that ended. Then, 27 years later, it made its presence felt once more. Investors got swept up in the ‘you can’t go wrong buying’ frenzy. What had gone up by 100% or 200% in a relatively short space of time, would continue to do so. No. No. No. That’s not how it works. The fate suffered by the Nifty Fifty was repeated in the Dotcom Bubble Bust… Here’s how the household names of the dotcom era performed during the bubble deflation period…the whooshing sound you can hear is the air coming out of the bubble pricing afforded to these ‘market darlings’… OK. OK. I know it’s different this time. People are wiser and won’t make the same mistakes. AI is going to be the big gamechanger…sounds just like what they said about radio in 1929. But that overhyped narrative didn’t stop RCA (Radio Corporation of America) from falling in price from US$549 to US$15 in 1932…an unbelievable (and, in mid-1929, an inconceivable) 97% loss of value. Which brings us to this bubble’s next big thing… Nvidia…has the look and feel of 1929 and 1987 Amongst the Magnificent Seven’s stellar 2023 performance, Nvidia’s has been the real headline grabber. Up almost 200%...that’s also unbelievable. A large chunk of AI manic has been channelled into this one stock. This next chart, courtesy of Momentum Structural Analysis (MSA), shows how the share price of Nvidia was in a steady uptrend, then POW, it broke out into ‘distribution range’ (red box). According to Michael Oliver (CEO and founder of MSA), this distribution range is when buyers and sellers have a bit of an arm wrestle. Then, the buyers gain the upper hand, and the price shoots out of the distribution range. And, just to prove that when it comes to human nature, everything old is new again, here’s the same pattern repeated prior to the 1929 and 1987 crashes… Last week I recorded a chat with Michael Oliver for members of The Gowdie Advisory and he said to me that if Nvidia falls back into the ‘distribution range’, then watch out. Where’s the top of the ‘distribution range’? Just over US$400. What price did Nvidia close at last night? US$406. If history is any guide, it looks like things are going to get very interesting on Wall Street. Regards,

Vern Gowdie,

Editor, The Daily Reckoning Australia

Advertisement: Jim Rickards: This year the economy will be slammed into ‘full reverse’ Here’s what you need to know...and how you can prepare...for the biggest geoeconomic shift of our lifetime... Click Here |

|

| | By Bill Bonner | | Editor, The Daily Reckoning Australia |

|

Dear Reader, What an exciting weekend…with the fight of the century! On Saturday, the Wagnerians were on the road to Moscow to confront Putin. By Sunday, a ‘deal’ had been worked out. But we’re talking about something much more amusing, the upcoming battle between Elon Musk and Mark Zuckerberg. The two ultra-billionaires, both serious martial art enthusiasts, were set to square off after Musk — supposedly prompted by Zuckerberg’s move to compete with Twitter — issued a challenge. It was probably a joke; Musk proposed a ‘cage match’. Zuckerberg shot back ‘send me location’. So, the fight is on…maybe. We hope so. It would be entertaining. And extremely lucrative for everyone involved — ringside seats, hotel bookings, broadcast rights, T-shirts and memorabilia…it would probably be the single most profitable event in history. Vegas odds-makers are going 3-2 for Musk. Gentlemanly combat Settling rivalries with a battle of champions is a venerable way to spare the money and lives that would be lost in a real battle. It’s also much more honourable. In the Bible, David and Goliath faced each other single-handedly. So did Achilles and Hector in Homer’s Iliad. Typically, the cost of war is borne by those who are least responsible for it — taxpayers and draftees. Instead, why not just let the deciders settle it on live TV…and make a profit on it? Zelenskyy and Putin, for example, are fighting over who controls the eastern section of Ukraine, traditionally a ‘borderlands’ area. How about a cage match? While disputes between nations are often resolved by force, elections are usually a matter of fraud. ‘He’ll keep us out of war’, promised supporters of Woodrow Wilson. ‘He’ll create a Great Society’, they pledged for Lyndon Johnson. ‘He’ll make America great again’, they vouchsafed on Donald Trump’s behalf. Once elected, the president then undertakes to reward his campaign donors. Voters are often forgotten or stabbed in the back. Think about how much expense, corruption, and bombast could be avoided by replacing national elections with cage matches. Hillary versus Donald…Donald versus Joe. Who knows which way these rumbles would go…but they could hardly be worse than the verdict of the voters. Back on the beat But let’s move on…the Fed has paused. Stocks are still high. Unemployment is still low. And the credit catastrophe, if there is one, is still ahead. As to the coming catastrophe…David Rosenberg, former head economist at Merrill Lynch, is on the case. DNyuz: ‘He…cautioned that investors appear overly optimistic today, just as they were nearly 25 years ago. For example, they’ve roughly tripled Nvidia’s stock price this year, lifting its market capitalisation to north of US$1 trillion. They’ve also more than doubled the stock prices of Tesla, Meta, and other popular tech names too. ‘“The smug complacency in 2000 looks eerily similar to what we have on our hands today,” Rosenberg said, adding that a recession is “coming sooner than you think.” ‘He noted the inverted yield curve is signalling a 99% chance of a recession, and based on past economic cycles, that may mean the downturn arrives before the end of this year.’ Speculators so loved US commercial real estate…and were so sure that the lowest interest rates in 5,000 years would stick around for years more…that they looked to make easy money buying property in the heart of the US’s most dynamic cities. For an entire generation, they were in the money. Interest rates went down. The players could refinance…and refinance…even ‘taking out equity’ as the price of the buildings went up while interest rates went lower. Then, in 2009, the Fed began a ‘zero interest rate’ policy…holding its key lending rate below the rate of inflation for most of the next 14 years. It was a dream come true for leveraged real estate speculators. ‘Extend and Pretend’ But now, they face a ‘whole new ballgame’. Bloomberg reports: ‘The World’s Empty Office Buildings Have Become a Debt Time Bomb’: ‘In New York and London, owners of gleaming office towers are walking away from their debt rather than pouring good money after bad. The landlords of downtown San Francisco’s largest mall have abandoned it. A new Hong Kong skyscraper is only a quarter leased. ‘…the trouble in property is set to play out for years.’ Bloomberg continued: ‘The “Extend and Pretend” Real Estate Strategy Is Running Out of Time’: ‘It’s not that the market participants had forgotten the lessons of the global financial crisis that followed the 2000s boom. It’s that they remembered them. Faced with delinquent loan payments, lenders decided to be patient: Instead of foreclosing on properties whose value was plummeting, they lengthened loan terms and ignored short-term valuations. They called it “extend and pretend”…’ In the commercial property slump of 1992, for example, Donald Trump was nearly ruined. He was as much as US$900 million in the hole. But extending and pretending worked for him as it did for others. The Fed was committed to low interest rates…and the bull market in bonds (with lower and lower yields) that began in 1982 was only about half over. As rates went down, the value of properties went up — especially in New York. By 2016, when he ran for president, Mr Trump said he was worth US$10 billion. So, it was no accident that he told the Fed to cut rates when he got into the White House. He was a ‘low-interest rate guy’, he said. As long as the bear market in yields (falling interest rates/rising bond prices) continued, you could survive a tight real estate market just by maintaining your cool. You refinanced…and waited for the buyers/renters to come back. But what about now? Stay tuned… Regards,

Bill Bonner,

For The Daily Reckoning Australia Advertisement: Resource ‘MELT UP’ dead ahead? A new wave of resource chaos could be about to set off a chain reaction of shortages…panic buying…sudden price spikes…and profit opportunities. So says veteran geologist James Cooper. But this time around, it won’t be lithium, nickel, or LNG stocks at the heart of the story. But a new class of Aussie-listed mining stocks that James suggests you scoop up BEFORE the anticipated shortages hit. Which plays should you be looking at, exactly? Click right here and see. |

|

|