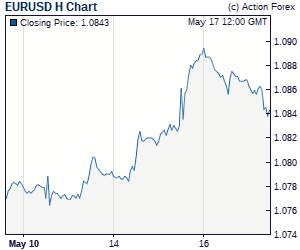

Asian markets are weighed down slightly by a batch of soft economic data from China, but loss is limited so far. At the time of writing, China Shanghai SSE is down -0.47% and stays above 2800 key level throughout the session. Hong Kong HSI is down -0.17%. Singapore Strait Times is down -0.84%. Nikkei is on holiday today. In the currency markets, Yen is trading broadly lower with EUR/JPY and GBP/JPY breached last week's highs. Dollar also weakens mildly as recent near term consolidation is set to extend with another pull back. Sterling is trading as the second strongest one for today. But it's going to face a look of political an data risks ahead in the week. Asian markets are weighed down slightly by a batch of soft economic data from China, but loss is limited so far. At the time of writing, China Shanghai SSE is down -0.47% and stays above 2800 key level throughout the session. Hong Kong HSI is down -0.17%. Singapore Strait Times is down -0.84%. Nikkei is on holiday today. In the currency markets, Yen is trading broadly lower with EUR/JPY and GBP/JPY breached last week's highs. Dollar also weakens mildly as recent near term consolidation is set to extend with another pull back. Sterling is trading as the second strongest one for today. But it's going to face a look of political an data risks ahead in the week. Released in Asian session, China GDP growth slowed to 6.7% yoy in Q2, down from 6.8% yoy and met expectation. Industrial production growth slowed to 6.0% yoy in June, down from 6.8% yoy and missed expectation of 6.5% yoy. Fixed assets investment growth slowed to 6.0% yoy, down from 6.1^ yoy and missed expectation of 6.2% yoy. Retail sales offered a brighter spot as they grew 9.0% yoy, up from 8.5% yoy and matched expectations. Eurozone trade balance will be featured in European session. But major focus will be on US retail sales, and Empire state manufacturing index. Technically, as we pointed out in the weekly report that Dollar's up trend is not ready to resume yet. We'll likely see more pull back against Europeans, and possibly against Australian Dollar too. But we're not anticipate steep selloff there. Two Euro crosses are worth a watch today. EUR/GBP's rally attempt failed last week but it's staying above 0.8808 minor support, thus retaining near term bullishness. However break of 0.8808 will be a sign of near term bearish reversal. Similar, despite all the volatility, EUR/AUD is holding above 1.5696 minor support and stays near term bullish. But a solid break of this support level will also be a sign of near term bearish reversal. |