| -- | December 12, 2017 Why Bitcoin Can’t Be Money By Patrick Watson Everyone is talking about bitcoin, even people who otherwise know little about investing. That’s probably a bad sign for bitcoin. Recently, I had a conversation with my 89-year-old father. He likes reading newspapers, so this year I got him a Wall Street Journal subscription. Now he’s up on the financial news. A few weeks ago, he asked the big question: “What is bitcoin?” I told him what I knew: Bitcoin is a digital currency, designed to be scarce, anonymous, and secure, that it’s price has gone vertical, that some people think it will one day replace dollars. He was with me until that last part. A private, digital-only currency didn’t make sense to him. I pondered that conversation driving home… and I think he was right. Bitcoin may be useful and valuable, but it won’t replace fiat currencies anytime soon.

Photo: Getty Images Power Mining Before we talk about bitcoin, I want to let you know that our Mauldin Economics VIP offer is still open until December 13. VIP gives you access to all our premium investment services, including my own Yield Shark and Macro Growth & Income Alert, for one low price. It also comes with some other perks—get all the details here. Now, on with our topic. Unless you’ve been hiding under a rock, you know bitcoin prices have gone bananas. I’m not even going to quote any numbers. Anything I say will be laughably wrong by the time you read this. Could some virtual currency that only exists on a computer screen really be worth these crazy prices? Maybe. If you think it will become a major medium of exchange, bitcoin is far underpriced. That’s a big “if” we’ll discuss in a minute. First, let’s look at some more practical issues. Bitcoins enter the digital world when someone “mines” them by solving certain math problems. Mining operations have turned from college students sitting at their laptops to huge enterprises that use massive computing power to run ever more complex math calculations. Some of the computers dedicated to solving those math problems fill entire buildings.

Photo: Getty Images Bitcoin’s anonymous inventor, who called himself Satoshi Nakamoto, built scarcity into the system. Mining gets more difficult as time passes and the supply increases. No one will ever hit a mother lode and double the bitcoin supply overnight. As the math gets more complicated and the computers have to work harder, bitcoin mining consumes an increasing amount of electricity. And that’s starting to be a problem. Here’s science writer Eric Holthaus at Grist last week: In Venezuela, where rampant hyperinflation and subsidized electricity has led to a boom in bitcoin mining, rogue operations are now occasionally causing blackouts across the country. The world’s largest bitcoin mines are in China, where they siphon energy from huge hydroelectric dams, some of the cheapest sources of carbon-free energy in the world. One enterprising Tesla owner even attempted to rig up a mining operation in his car, to make use of free electricity at a public charging station. That’s pretty crazy, but it gets crazier. In just a few months from now, at bitcoin’s current growth rate, the electricity demanded by the cryptocurrency network will start to outstrip what’s available, requiring new energy-generating plants. And with the climate conscious racing to replace fossil fuel-based plants with renewable energy sources, new stress on the grid means more facilities using dirty technologies. By July 2019, the bitcoin network will require more electricity than the entire United States currently uses. By February 2020, it will use as much electricity as the entire world does today. This is an unsustainable trajectory. It simply can’t continue. Not to put too fine a point on it, but this is bonkers. I have not independently verified these claims. In the comments section at the bottom of Eric’s article, many expert-sounding people dispute them. So maybe he’s wrong. | - |  | Until December 13, you have a chance to become a Mauldin VIP... And get the entire Mauldin Economics team behind your portfolio... At up to a 74% discount Want in? |

| | - |

Still, the broader point seems right. Bitcoin mining and transaction processing consumes a lot of power, and we don’t have infinite amounts of it. A trend that can’t continue, won’t—so something will change it. Here’s a partial list of possibilities: - Computers could get faster and more energy efficient

- We could find new sources of cheap, abundant electricity

- Bitcoin’s price could fall and make mining unprofitable

- Another, less energy-consuming cryptocurrency could take bitcoin’s place

- Governments could try to outlaw bitcoin and shut down the miners

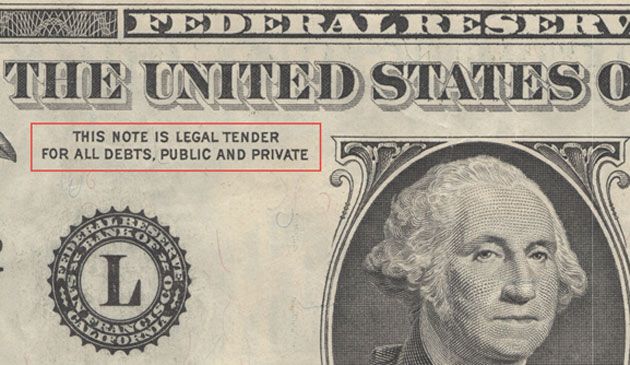

Of those, government interference is probably bitcoin’s greatest threat. Governments don’t like the anonymity, because it facilitates tax evasion, money laundering, smuggling, and other illegal acts. But there’s something even more basic to consider... What Is Money? You can’t talk about bitcoin for long before you get to the “What is money?” question. My favorite answer: Money is simply the most liquid asset in a given place and time. Almost everyone accepts it as payment because they trust it, and they trust it because they know others accept it. Could bitcoin or another cryptocurrency ever reach that status? Maybe, but it will have to cross a very wide moat. Pull a Federal Reserve Note from your wallet. Look closely and you’ll see a legend about legal tender:

Photo: Mises Institute Your dollar bill is legal tender for all debts, public and private. The government says everyone must accept it, so we do. Nothing prevents us from accepting other currencies as well. You can trade chickens for cows, or vice versa, if everyone agrees. But you’ll still have to report any taxable gain in dollar terms and pay tax in dollars. That’s the “public” part of the legal-tender legend. In the modern world, governments define money because they have the raw power to define how you must pay your taxes. They can and will use force to make you pay—and deadly force if you resist too hard. The IRS doesn’t accept cows, chickens, yen, gold, or bitcoin. It demands dollars. Don’t have any? Get some or go to prison.

Photo: Getty Images As long as we pay a significant part of our income in taxes, - We must all own whatever currency the government accepts as payment, in quantities sufficient to pay our tax obligations.

- Business accounting must use government-dictated currency as the unit of account.

That means most people will default to using the same currency for personal spending and investing. This gives government-issued money an automatic advantage over bitcoin or any other competitor. When national governments start accepting bitcoin for tax payments, you can fairly call it “money.” Until then, it’s simply another risk asset like gold, stocks, or pork bellies. Is bitcoin a risk asset you should own? Probably not, unless you are prepared for some serious pain whenever the price heads south. I don’t know when that will happen. Bubbles get way bigger than anyone thinks possible, but at some point, they all pop. This one will too. See you at the top,  Patrick Watson P.S. If you’re reading this because someone shared it with you, click here to get your own free Connecting the Dots subscription. You can also follow me on Twitter: @PatrickW.  | Subscribe to Connecting the Dots—and Get a Glimpse of the Future

We live in an era of rapid change… and only those who see and understand the shifting market, economic, and political trends can make wise investment decisions. Macroeconomic forecaster Patrick Watson spots the trends and spells what they mean every week in the free e-letter, Connecting the Dots. Subscribe now for his seasoned insight into the surprising forces driving global markets. |

Senior Economic Analyst Patrick Watson is a master in connecting the dots and finding out where budding trends are leading. Patrick is the editor of Mauldin Economics’ high-yield income letter, Yield Shark, and co-editor of the premium alert service, Macro Growth & Income Alert. You can also follow him on Twitter (@PatrickW) to see his commentary on current events. Senior Economic Analyst Patrick Watson is a master in connecting the dots and finding out where budding trends are leading. Patrick is the editor of Mauldin Economics’ high-yield income letter, Yield Shark, and co-editor of the premium alert service, Macro Growth & Income Alert. You can also follow him on Twitter (@PatrickW) to see his commentary on current events.

Share Your Thoughts on This Article

Use of this content, the Mauldin Economics website, and related sites and applications is provided under the Mauldin Economics Terms & Conditions of Use. Unauthorized Disclosure Prohibited The information provided in this publication is private, privileged, and confidential information, licensed for your sole individual use as a subscriber. Mauldin Economics reserves all rights to the content of this publication and related materials. Forwarding, copying, disseminating, or distributing this report in whole or in part, including substantial quotation of any portion the publication or any release of specific investment recommendations, is strictly prohibited.

Participation in such activity is grounds for immediate termination of all subscriptions of registered subscribers deemed to be involved at Mauldin Economics’ sole discretion, may violate the copyright laws of the United States, and may subject the violator to legal prosecution. Mauldin Economics reserves the right to monitor the use of this publication without disclosure by any electronic means it deems necessary and may change those means without notice at any time. If you have received this publication and are not the intended subscriber, please contact service@mauldineconomics.com. Disclaimers The Mauldin Economics website, Yield Shark, Thoughts from the Frontline, Patrick Cox’s Tech Digest, Outside the Box, Over My Shoulder, World Money Analyst, Street Freak, Just One Trade, Transformational Technology Alert, Rational Bear, The 10th Man, Connecting the Dots, This Week in Geopolitics, Stray Reflections, and Conversations are published by Mauldin Economics, LLC. Information contained in such publications is obtained from sources believed to be reliable, but its accuracy cannot be guaranteed. The information contained in such publications is not intended to constitute individual investment advice and is not designed to meet your personal financial situation. The opinions expressed in such publications are those of the publisher and are subject to change without notice. The information in such publications may become outdated and there is no obligation to update any such information. You are advised to discuss with your financial advisers your investment options and whether any investment is suitable for your specific needs prior to making any investments.

John Mauldin, Mauldin Economics, LLC and other entities in which he has an interest, employees, officers, family, and associates may from time to time have positions in the securities or commodities covered in these publications or web site. Corporate policies are in effect that attempt to avoid potential conflicts of interest and resolve conflicts of interest that do arise in a timely fashion.

Mauldin Economics, LLC reserves the right to cancel any subscription at any time, and if it does so it will promptly refund to the subscriber the amount of the subscription payment previously received relating to the remaining subscription period. Cancellation of a subscription may result from any unauthorized use or reproduction or rebroadcast of any Mauldin Economics publication or website, any infringement or misappropriation of Mauldin Economics, LLC’s proprietary rights, or any other reason determined in the sole discretion of Mauldin Economics, LLC. Affiliate Notice Mauldin Economics has affiliate agreements in place that may include fee sharing. If you have a website or newsletter and would like to be considered for inclusion in the Mauldin Economics affiliate program, please go to http://affiliates.ggcpublishing.com/. Likewise, from time to time Mauldin Economics may engage in affiliate programs offered by other companies, though corporate policy firmly dictates that such agreements will have no influence on any product or service recommendations, nor alter the pricing that would otherwise be available in absence of such an agreement. As always, it is important that you do your own due diligence before transacting any business with any firm, for any product or service. © Copyright 2017 Mauldin Economics | -- |