| Debt Ceiling or Trap Door? |

Tuesday, 6 June 2023 — Gold Coast  | | By Vern Gowdie | | Editor, The Daily Reckoning Australia |

|

[6 min read] | Quick summary: Watching President Biden and Speaker of the House, Kevin McCarthy’s charade of acting responsibly, while giving the green light to another two years of unfettered and wasteful spending, was nauseating. All that Biden and McCarthy have done is buy (or, should that be, borrowed) more time. The massive debt problem is NOT going away, just deferred. Read on… |

|

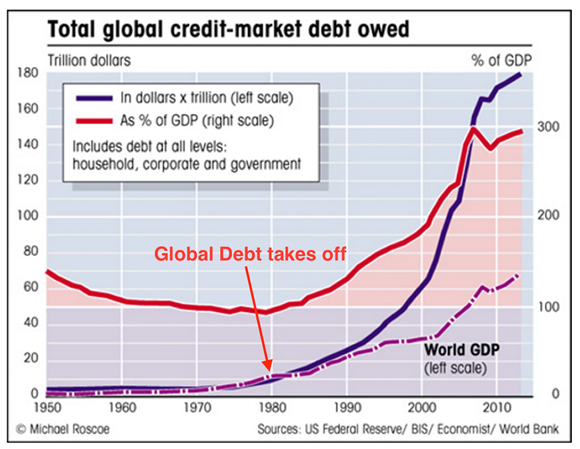

Dear Reader, Watching President Biden and Speaker of the House, Kevin McCarthy’s charade of acting responsibly, while giving the green light to another two years of unfettered and wasteful spending, was nauseating. Does anyone buy the BS these guys are selling? Surely not? Insincerity oozes out of their every pore. All that Biden and McCarthy have done is buy (or, should that be, borrowed) more time. The massive debt problem is NOT going away, just deferred. Pass the borrowed buck to another administration to fix. For now, we’ll keep doing what we’ve done for the past four decades…spend more than we earn and pretend we are acting responsibly. Did the clowns in Washington bother to read the article Reuters published on 17 May 2023? The one that alerted us to the enormity of the global debt load (emphasis added): ‘A measure of debt across the globe rose in the first quarter to almost $305 trillion, and the rising cost to service that debt is triggering concern about the financial system's leverage, a widely tracked study showed. ‘The Institute of International Finance, a financial services trade group, said on Wednesday global debt rose by $8.3 trillion in the first three months of this year compared to the end of 2022 to $304.9 trillion, the highest since the first quarter of last year and second-highest quarterly reading ever.’ As a point of reference, global debt in 2008 (when the world went to the brink of a full-blown debt crisis) was around…US$140 trillion. Wow. In the space of 15 years, we have more than doubled global debt and continue to delude ourselves into believing we can go on our way without there being any consequences. Seriously, how stupid can society be? I’m not sure whether it’s listening to the claptrap from these so-called leaders of the free world or the thought of the hardship that waits for my children that has me reaching for the bucket. Strains are global To be fair, monetary madness is not isolated to the US. The debt disease has spread to all corners of the world. Fitch Ratings recently highlighted growing concerns over the Old Continent’s debt load… To quote from the article: ‘Europe’s biggest economies will struggle to cut debt this year, leaving their borrowings still significantly higher than before the pandemic struck, according to Fitch Ratings.’ And it’s not just the debt load that’s higher…so too are the debt servicing costs. The heady days of European sovereign debt being issued at negative rates (can you believe how stupid that era was?) are long gone. Benchmark borrowing costs in the Eurozone are now around 3.25%. What’s happening in the US and Europe is being echoed in China’s heavily indebted local government sector…

As reported by Bloomberg, one of the major pillars upon which China’s economic fortunes rests, Local Government Financing Vehicles (LGFVs), are under pressure:

‘Financial stress faced by China’s local governments is limiting fiscal support for the economy’s recovery, with half of cities experiencing difficulty in managing the interest payments on their debt last year. ‘That’s according to a report by Rhodium Group researchers, who examined annual reports from 205 Chinese cities and nearly 3,000 local government financing vehicles, or LGFVs, the state-owned companies that carry out infrastructure investment.’

It’s evident, with the normalising of interest rates, that the world is finding it a struggle to meet commitments on current debt loads.

On what planet do people think adding to this debt load — with tens of trillions of dollars in more loans — is going to end well?

Well, sadly for us, that planet is…Earth.

How we got here…in pictures

Here’s an ‘Around the World in 80 seconds’ pictorial of how we got to this point of insanity and why things are going to get far worse before the market forces compel future political leaders to act decisively.

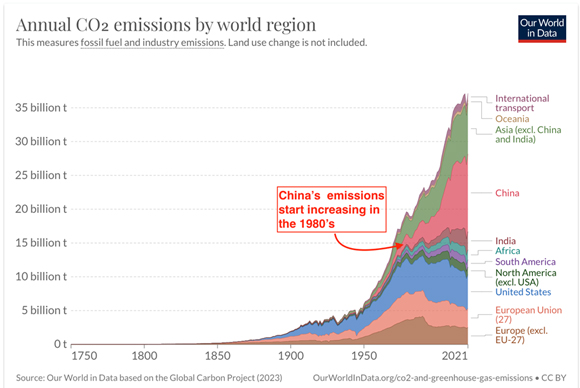

The timing of China’s decision to modernise its society in the late 1970s/early1980s was perfect.

Interest rates peaked in the early ’80s.

Falling rates enabled the developed world to borrow more (and, more) money.

The borrowed funds were primarily used for consumption and making unfunded promises to secure electoral victories.

China’s low-cost manufacturing base exported low inflation (which resulted in lower interest rates) and low wages (resulting in the need to borrow more to maintain living standards) around the world.

Producing all those material goods for (debt-funded) Western consumption required more mining, factories and transportation. Therefore, it should come as no great surprise to see China’s CO2 emissions increase significantly after 1980. With developed world GDP growth ticking along at an annual clip of around 4% (thanks to the infusion of debt into the system to boost headline GDP numbers), more expansive welfare and healthcare promises were made…

So, here we are four decades later. - Global growth is slowing (due to debt loads).

- Populations are ageing…more health care and welfare costs.

- Social spending promises are widely regarded as irrevocable entitlements.

- Whether we like it or not, we are committed to funding a multi-multitrillion-dollar campaign to reduce CO2 emissions.

- Our once friendly and mutually beneficial ‘Chinese maker and Western taker’ arrangement is under considerable strain.

This grand experiment in living off the ‘never, never’ must surely be in its final stages. If something cannot continue, then it won’t. At some point — possibly in the next few years — one straw too many is going to be added to the back of this 40-plus-year-old economic camel. Ironically, the one upside of an abandonment of the debt-funded economic growth model will be…less CO2 emissions. I wonder if the climate change zealots will be cheering this outcome. Lifting the debt ceiling has taken us one step closer to the economic trapdoor. Shame on them. Regards,

Vern Gowdie,

Editor, The Daily Reckoning Australia

Advertisement: Jim Rickards: In the next few months of 2023, the economy will be slammed into ‘full reverse’. Here’s what you need to know...and how you can prepare...for the biggest geoeconomic shift of our lifetime... Click Here |

|

| | By Bill Bonner | | Editor, The Daily Reckoning Australia |

|

Dear Reader, Last week we watched the debt ceiling go up and the AI bubble expand. The first was inevitable. The second…entertaining. The debt ceiling shootout was fake. The characters had no reason to go gunning for each other. This was the one issue on which they were all in agreement — the Feds should borrow more money. Everybody knew how it would end, too — in a slimy compromise of some sort. Still, it was even slimier than we expected. The Republicans, supposedly, were using the ceiling to pry loose some concessions that would appeal to their supposedly ‘conservative’ base. As it turned out, they got nothing. And nobody cared anyway. It was theatre. But bad theatre. The characters were shiftless and phony. The dramatic tension was false. And there were no surprises. And now debt will continue to grow untouched. Artificial exuberance Meanwhile, this is not the first time that we’ve seen a tech bubble…what is a little surprising is that we’re seeing one now. And it is one of the best. Charlie Bilello reports: ‘The exuberance over generative artificial intelligence had been building throughout earnings season, with 190 mentions of the word “AI” in earnings calls for the largest tech companies versus just 36 mentions a year ago. ‘And then Nvidia reported earnings, transforming the AI boom into a full-fledged mania. While Q1 revenues were actually down 13% year-over-year, all the attention was on forward guidance. Nvidia said revenues in the current quarter would hit $11 billion, a new record high for the company (prior high was $8.3 billion) and 50% above wall street estimates.’ Nvidia jumped by 25% last week…putting it in the trillion category and erasing all last year’s losses. What is unusual about this mania is that it takes place in the wrong season. Like a young Frenchman reaching adulthood in 1914 and doomed to the army, the AI mania has a short life expectancy. A tale of two streets Typically, the stock market flourishes when credit flows. That is what happened in the 2009–22 bubble. The Fed lent out money below the rate of inflation — lots of it. In 2009, the Fed balance sheet — a measure of its lending — stood at less than US$900 billion. By 2022, it was almost over US$9 trillion. Most of this money went out to the big banks and to their big financial borrowers on Wall Street. They made their bets…driving up asset prices. The Nasdaq, home of much hope and wishful thinking, rose in line with Fed lending, up from 1,300 in 2008 to 13,000 in 2021. This increase in prices did not represent an increase in values. While Wall Street headed to the Moon, the Main Street economy limped along on Earth with some of the lowest growth rates since the Great Depression. Asset prices are a claim on things in the real world. If you own a factory, for example, you should be able to sell it for about 10 times the net value of its output. That’s the connection between Wall Street and Main Street — values on Wall Street should represent the expected stream of earnings on Main Street from selling real goods and services. They are meant to rise and fall together. But now, Wall Street prices represent trillions of dollars’ worth of output that hasn’t yet been put out and never will be. At 38 times sales, for example, Nvidia is extremely unlikely to produce enough profits to make the stock price reasonable. Even with a 100% profit margin (impossible)…and a 100% dividend payout (never going to happen)…at the current price, it would take until 2061 for investors to get their money back. A 180-degree shift The outlook for a bubble is never good. All bubbles pop. And all booms built on central bank credit eventually go back whence the money came — to nowhere. But the outlook for this bubble is particularly bad. The timing is off. The Fed’s key rate is about zero, in real terms, after being as much as 6% negative in 2022. Neither is the Fed’s balance sheet ripping skyward as it did during the last bubble epoch. Instead, the money supply is now falling at the fastest rate in history. Here’s Charlie Bilello again: ‘After a 40% increase in 2020–21, we’ve seen a 180-degree shift. The US Money Supply has fallen 4.6% over the last 12 months, the largest year-over-year decline on record (note: M2 data goes back to 1959).’ There is a season for everything. And this is not the season for a real mania. So, here’s a prediction: either the Fed puts more money into the system…or the AI bubble dies in the trenches. Regards,

Bill Bonner,

For The Daily Reckoning Australia Advertisement: Geologist shoots weird video in bush He’s a 15-year mining veteran… And he just hired a film crew, headed out to the bush…to share an unusual message about the resource markets. Is he on to something? Or is he losing it? Check out the footage HERE — then decide. |

|

|