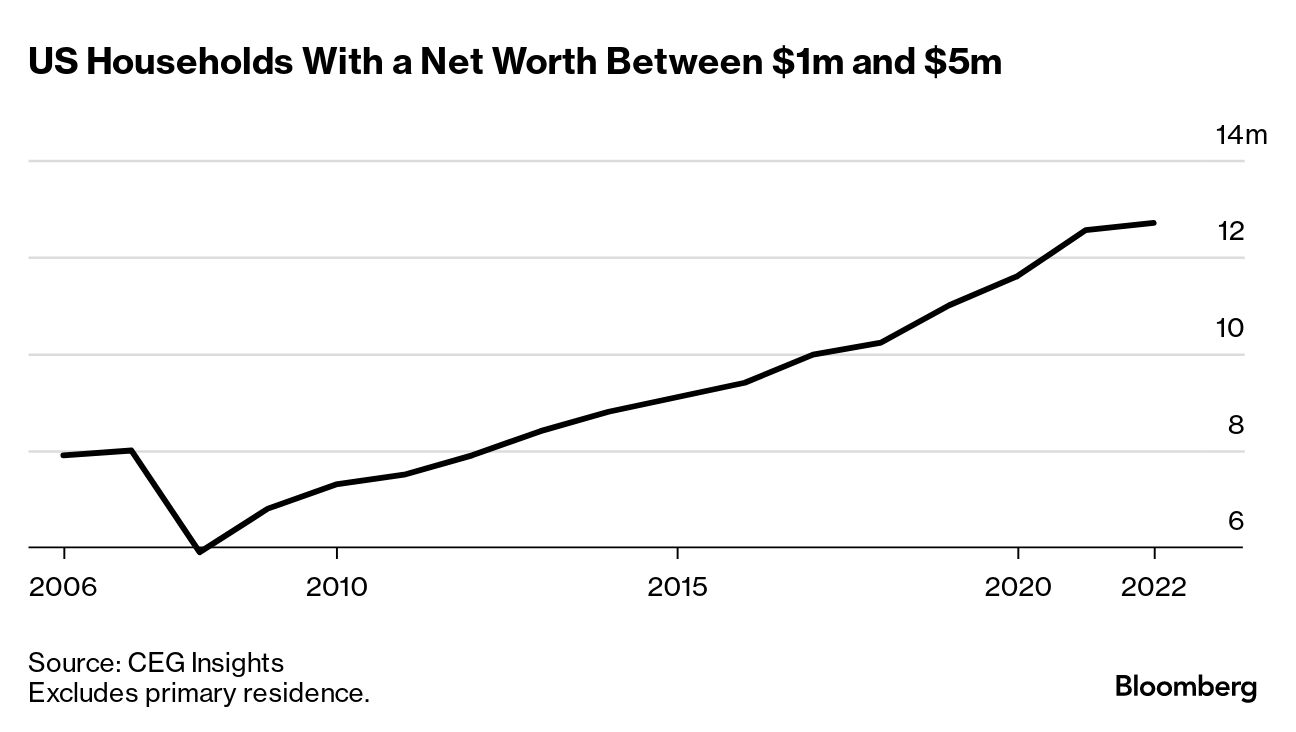

| UBS Group reported stronger-than-expected client inflows in its wealth-management business, boosted by the first signs of stabilization at Credit Suisse as it carries out the complex integration of its rival. The unit saw net new money of $22 billion in the third quarter compared with an estimate of $14 billion. About $3 billion of that was at Credit Suisse’s wealth arm—its first positive client flows in a year and a half. Still, the Zurich-based bank posted a net loss of $785 million for the three months to September, its first quarterly loss in almost six years thanks to the expense of absorbing its purchase. UBS has signaled it will shutter roughly two-thirds of Credit Suisse’s investment bank, including almost all its trading operations. The bank is seeking to save money by firing employees as it combines the two workforces. The number of workers fell by more than 4,000 in the third quarter and is down by about 13,000 against the total figure the two banks would have had as a combined entity at the end of last year. UBS Chief Executive Officer Sergio Ermotti said the bank is in “full execution mode” around the integration. —David E. Rovella Fear is everywhere. Fragile markets, shadow lenders, international tensions and too many wars—global bankers gathering in Hong Kong were meant to discuss how they’re adapting to the financial world’s “complexity” and ended up dwelling on the potential for big blowups instead. Deutsche Bank CEO Christian Sewing said “my biggest fear is there’s one more geopolitical escalation and there’s a market event.” A neighbor of Ukraine gave a warning to a distracted West: The nation’s allies must stand firm in backing Kyiv or risk emboldening populist forces across Europe with a victory for Vladimir Putin. That from Romania Prime Minister Marcel Ciolacu, who told Bloomberg News his government will forge ahead with “multi-dimensional support” for Ukraine even as European allies show signs of war fatigue, particularly with the Israel-Hamas conflict overshadowing a Russian invasion that’s estimated to have killed more than 100,000 people. Israeli officials meanwhile said their forces are fighting inside Gaza City while Prime Minister Benjamin Netanyahu said his country could keep control over Gaza for an “indefinite period,” suggesting a longer-term role in a besieged territory where health officials say more than 10,000 people have been killed by Israeli attacks. The war began a month ago following a Hamas assault that Israel officials said killed 1,400 people and resulted in hundreds of hostages being taken to Gaza. Amid calls for a ceasefire, Netanyahu said the hostages must be released first.  Marcel Ciolacu, Romania's prime minister, during an interview at the Victoria Palace in Bucharest on Nov. 6. Photographer: Andrei Pungovschi/Bloomberg US officials will seek to limit access to Federal Home Loan Banks after failing lenders turned to the $1.3 trillion system in desperate bids to survive March’s regional banking bloodbath. The Federal Housing Finance Agency will try to push FHLBs back to their roots in housing finance, and away from serving as lenders of last resort to troubled banks. The commercial real estate crisis finally claimed a widely expected victim: WeWork. At its 2019 peak, the office space disruptor commanded a $47 billion valuation. Now, in its bankruptcy filing, it lists $19 billion of liabilities and just $15 billion of assets. And it cost this man $11.5 billion. Private equity companies have long sought to attract clients with as little as $5 million in investable assets. For the biggest names in the field (think Apollo, Ares, Blackstone, KKR), the next prize is those with $1 million to $5 million, a segment of US households that jumped close to 60% over the past 16 years. The race for these so-called mini-millionaires has intensified as pension funds and endowments, often over-allocated to private equity, back away. In a rare move, Apple hit pause on development of next year’s software updates for the iPhone, iPad, Mac and other devices so that it could root out glitches in the code. The delay was meant to help maintain quality control after a proliferation of bugs in early versions. Rather than adding new features, company engineers were tasked with fixing the flaws and improving the performance of the software. At the Atlantic resort of Punta del Este in Uruguay, signs of an influx of wealthy residents are everywhere. The yacht club is now busy year-round, enrollment in private schools has swelled, and Italian developer Cipriani is breaking ground on what it says will be the “largest luxury complex in South America.” Wedged between Argentina and Brazil, Uruguay has long attracted wealthy visitors from both countries, especially during the summer months of December through February. But in recent years, more rich foreigners have been putting down stakes.  La Tahona, a gated community near Montevideo, Uruguay Source: La Tahona With Sam Bankman-Fried likely headed off to federal prison, attention now turns to a class-action lawsuit in Miami federal court by investors who claim they lost billions of dollars in his imploded crypto exchange, FTX. They pin the blame not only on the convict CEO and his inner circle, but also on celebrities who were paid to endorse it to the masses—as well as bankers, accountants and lawyers who propped it up.  Larry David, Sam Bankman-Fried and Tom Brady. Photographers: Kevin Winter/Getty Images; Yuki Iwamura/Bloomberg; Maddie Meyer/Getty Images Get the Bloomberg Evening Briefing: If you were forwarded this newsletter, sign up here to receive Bloomberg’s flagship briefing in your mailbox daily—along with our Weekend Reading edition on Saturdays. Bloomberg Green at COP28: World leaders will gather in Dubai on Dec.4-5 in an effort to accelerate global climate action. Against the backdrop of the United Nations Climate Change Conference, Bloomberg will convene corporate leaders, government officials and industry specialists from NGOs, IGOs, business and academia for events and conversations focused on creating solutions to support the goals set forth at COP28. Register here. |