| Part One: How to Structure Your Portfolio for a Fierce Bidding War Among the Majors |

Thursday, 20 April 2023 — Melbourne  | | By James Cooper | | Editor, The Daily Reckoning Australia |

|

[8 min read] | Quick summary: Today, James Cooper outlines why you should be preparing your portfolio for a fierce bidding war amongst the world’s largest mining companies. He outlines why the stage is set and how you can structure your portfolio to benefit. Read on to find out more… |

|

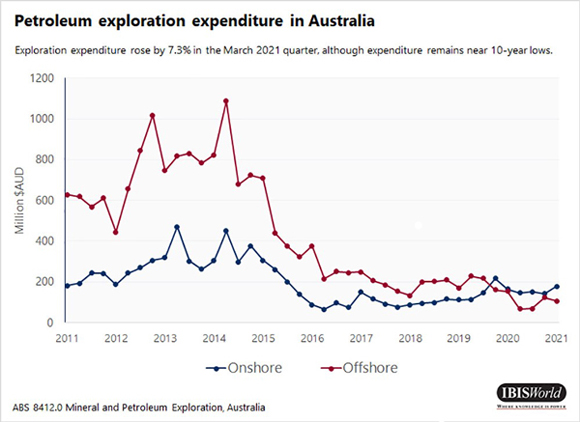

Dear Reader, Earlier this week, I wrote to my subscribers that small-time investors like you and me are the pesky flies that sit on the wall of big-time players and mining executives… Usually, we play ball on managements recommendations to shareholders. As deals get brokered…mergers and acquisitions (M&A) take place…investors are fed the corporate spin… But rumblings are growing in the industry. Are these deals always in the best interests of shareholders? Given much of the recent M&A activity has involved majors taking over mid-tier mining stocks, one has to ask: Is now really the time to be selling? With so many metrics pointing towards supply deficits and unprecedented demand arriving in the form of a dramatic energy transition, it seems we truly are embarking on a new era for commodity stocks. Fundamentally, the outlook for mining has never been stronger. Take yourself back to the early days of the China-fuelled commodity boom around 2003/04, and we perhaps have a sense of what lies ahead. The cycle is on course to repeat — not exactly, but with similar outcomes. But this time it’s the political elite leading the charge. Why? They’ve signed the death knell for the oil and gas industry. Termination of exploration rights, strict ESG requirements that cut investment to the industry from retail funds, and an open commitment to destroy their business model… That’s why new oil and gas discovery is at its lowest level in 75 years, according to the research firm Rystad Energy. The situation is similar in Australia. Oil and gas expenditure for new discoveries is hovering around 10-year lows. See for yourself below: Government mandates have successfully killed corporate motivation to find replacement fossil fuels. That has some very real consequences for our future energy security, when we ALSO consider mineral exploration has also suffered from severe underinvestment for more than a decade. It paints a VERY bleak picture for a SMOOTH energy transition. That’s the reality we now face. There’s no turning back now. With all that said, why are shareholders eager to give up their stock in a junior to a major mining corporation as part of a buyout offer? After all, it’s these mining conglomerates that are sounding the alarm bells over supply deficits. As Bloomberg reported late last year (emphasis added): ‘Glencore CEO Gary Nagle referenced estimates that global copper demand is expected to hit 50 million tonnes a year by 2030. In 2022, current world copper demand sits at around 25 million tonnes. ‘In short, Nagle believes that the combined forces of copper miners globally will not be enough to make up the shortfall soon enough to avoid an international copper supply deficit.’ Nagle would know…as the boss of a major international mining conglomerate, he sits at the coalface in terms of global copper production. With an international copper supply deficit looming, it seems bizarre — if not downright reckless — mining boards would recommend to shareholders that they accept an offer from a major. But that’s what the Oz Minerals [ASX:OZL] board did. A deal that was finally cemented last week. An insurmountable challenge awaits Forget about the exponential increases for metal supplies needed to bring about an end to oil… Maintaining current demand will be a challenge. The world’s most influential mining executives are acutely aware of this seemingly impossible task. Yet they have also compounded the problem… You see, the majors — burned by exuberant acquisitions at the peak of the last mining boom — have underinvested in project development and exploration for more than a decade. Instead of bringing new projects online, they’ve zipped the purse strings and carried on plunging machinery through marginal low-grade rock — material that would otherwise be considered waste. I’ve seen first-hand the slow-death effect of companies refusing to spend on project development while feeding marginal ore through processing facilities, pushing ageing facilities well past their use-by-dates. As Bloomberg reported earlier this month, the world’s largest copper-producing nation, Chile, just posted its LOWEST monthly copper output in six years. The state-owned copper conglomerate Codelco expects production to fall a staggering 7% this year. I’ve been warning my readers for months that Chile was staring down the barrel of a massive cut to its copper output. This reality is now hitting the headlines. It’s a key reason why one of our advanced copper explorers is up more than 60% since we recommended the stock four months ago. Lack of investment equals lack of supply. It’s a trend that will get worse, just as the world demands more copper. And not just copper, many other critical metals have suffered a similar fate…years of underinvestment. It brings me back to the question of acquisitions. Mines are a depleting asset. The world’s biggest miners desperately need to resupply their ageing mines. Lack of project development, inability to make meaningful investment in greenfield or brownfield exploration, rules out organic growth. But for stockholders of mid-cap miners holding quality high-grade deposits, this represents a long-term opportunity. Given the state of play, I firmly believe Oz Minerals shareholders will be kicking dirt for years to come…reeling from their missed opportunity, having given up their prized copper assets to BHP. But Oz should serve as an important lesson to ALL investors. The majors know what is at stake here. BHP co-owns the world’s largest copper mine, Escondida, in Chile. Last year, the big miner claimed lower ore grades, supply chain disruptions, and a reduced workforce due to COVID-19 impacted its FY22 copper production in Chile. But lower ore grade is the key. You can’t change the geology of a deposit. You also can’t find replacement ore in a snap. Higher prices will mean little for the likes of Glencore, Rio Tinto, or BHP if they can’t resupply their ageing mines. Prepare your portfolio for a fierce bidding war as the majors try to get their hands on the next generation of deposits. That’s what we are doing at Diggers and Drillers… Adding small- to medium- mid-cap mining stocks holding large, high-grade deposits. It’s these PRIZED assets that sit in the crosshairs of the world’s largest mining stocks. Using my industry experience and geological knowledge, I’ve been able to zero down on some of the best projects. Most of these stocks remain a BUY in the Diggers and Drillers portfolio. You can access all the details here. Next week, I’ll give you the name of one stock in our portfolio that is ALREADY the subject of a buyout offer from a major. I’ll also detail my strategy that led to the recommendation just a couple of months prior to the offer coming through. Until then, have a great week. Regards,

James Cooper,

Editor, The Daily Reckoning Australia

Advertisement: ‘The years ahead will be like

the mining boom on steroids’ …predicts Peter Milne in The Sydney Morning Herald. That true? Or just media fluff? And even if it IS true…is it worth sticking your neck out in such an uncertain market? We’ve recruited an experienced exploration geologist. He gives his verdict here. And talks specific stocks… |

|

| Don’t Cry for Central Banksters |

| | By Bill Bonner | | Editor, The Daily Reckoning Australia |

|

Dear Reader, Hola! Bienvenidos a Argentina! What did we learn from two months in a country with 100% inflation? ‘The most surprising thing’, says a friend, ‘is that it doesn’t seem to matter. The restaurants are full. People are spending money. Life goes on’. Our cab driver voiced much the same sentiment. ‘Yeah…it’s a crazy country. But we have good meat. Good vegetables. Pretty women. And Messi. [Argentina’s world champion soccer player.]’ ‘Yeah…’ he went on, after a moment of reflection…‘it’s nice here…but only if you have dollars’. Gresham’s law in action We confirm that a person with dollars can live well on the pampas. Our last night in Buenos Aires, for example, we went to the very popular restaurant Fervor in Recoleta. The place was packed with foreigners and locals. No wonder: the meat was among the best we’ve ever had. And with a good bottle of wine from Mendoza, the meal…the service…the ambiance — all were near perfect. A popular restaurant in a capital city is bound to be expensive. Compared to our dining in Salta, it was expensive. But at US$30 a person, compared to prices in New York or London, it was an incredible bargain. And that is true of many things — not tractor parts! — in most of the country. Almost everything is cheap…in dollars exchanged at the black-market rate. Great for foreigners. But this is just an example of a broader, more universal truth: the particulars matter. You may say that ‘all cats are the same’. But life for a scrawny alley cat in West Baltimore is very different from life for a pampered pet of the bourgeoisie in Harbor East. So too, even in a country with 100% inflation, some people live well. Many young people, for example, get paid in dollars…or Bitcoin [BTC]. Older people may rent out apartments or be able to raise prices in their businesses to keep up with inflation. Almost everyone spends pesos and keeps dollars. The upper classes have investments in the US and Europe. The lower classes buy bricks and mortar…adding spare rooms and garages, confident that no matter what happens to the peso, the concrete will still be there. Credit is almost impossible to get, so buildings go up a brick at a time, as owners spend their extra pesos. At today’s inflation rate, bricks double in price every year. But what about the US? And here is where looking back at Argentina may help us look ahead at the US. What we see is that when countries work themselves into an inflationary jam, inflation begins to look like the least of their problems. Panem et circenses For all the blah, blah on the subject, there are still only two possibilities. Either individuals decide for themselves what they want…and get it by ‘voting’ for it with their own money. Or someone else decides. The ‘someone else’ is always the big-mouth busybody who pretends to be selflessly acting on behalf of some greater good…some common good — equality, saving the planet, the Triumph of the Proletariat…Deutschland Uber Alles…or whatever. In Argentina, in 1919, Roque Saenz Pena, then president of Argentina, thought he had taken a giant step forward for mankind when he backed universal suffrage for all men. Not only did he allow them to vote, his Saenz Pena Law made voting mandatory. Then, a few years later, women too, were brought into the scheme. Opponents argued then that the masses lacked the education or the sophistication to vote intelligently. They were right. But the poor knew what they wanted. And, in 1946, for the first time in Argentine history, a candidate was able to win the Casa Rosada (equivalent to the White House) by promising to give them more of it. Juan Peron had a smile like an ad for toothpaste. And he could do maths. He quickly realised there were more poor voters than rich voters. And their votes were relatively cheap. The formula was such a hit, it ruled Argentina for the next seven decades as the country slid downhill, from the seventh richest nation on Earth…to number 86! What happened was no mystery…and no surprise. When you give away free stuff, you have to pay for it somehow. Peron taxed the rich. He taxed the middle classes. He taxed the productive parts of the economy and gave the goodies to the unproductive part. Output went down. But the demand for free stuff didn’t slack off. And soon, the tax base depleted, the politicians turned to borrowing. Tax, spend, borrow, default, print. The country has defaulted nine times. By 2001, Argentina defaulted on the biggest pile of debt ever — US$100 billion. When the loans gave out, the gauchos turned to the time-honoured scams of desperadoes everywhere: war and inflation. The first distracts the public; the second rips them off. In 1976, the generals staged a military coup and took power from Peron’s second wife, Isabelita. In 1982, they attacked the Falklands/Malvinas islands. By 1989, inflation was running hot — at 1,000%. Then, Carlos Menem restarted the cycle. The peso was pegged to the dollar, one to one. That emboldened borrowers to borrow and lenders to lend. Pretty soon, they had borrowed too much…and the one-to-one peso/dollar peg blew up. Then, prices rose again. When we first came to the pampas, the exchange rate was one-to-one, and Menem was in the Casa Rosada. Then, a couple of years later, in the early 2000s, the rate had gone to three-to-one. Skip ahead to this year — and we were getting almost 400 pesos per dollar. Loco locals Why don’t the Argentines put a stop to the spend-borrow-default-inflate cycle? Because once you get into it, the only way to stop it is financially painful — with recession/depression/bankruptcies/unemployment etc. But the real reason it goes on is because it becomes almost impossible, politically, to stop it. First, the masses want free stuff. Later, they depend on the free stuff. That’s why the US — where ‘transfer payments’ have gone up 290 times since 1954 — will find it almost impossible to stop the cycle too. But the most charming (and loco) thing about Argentine finance is the way people are willing to let bygones be bygones. Yes, Argentina is a serial defaulter. But that didn’t stop the country, in 2017, from selling more than US$2 billion worth of 100-year bonds. If history is any guide, investors will get wiped out…not once, but several times, as the government will default five times before they mature. So, what do we take from this experience…Argentina’s history…and our own history with it over the last 25 years? An inflation-and-default prone financial system is not the end of the world. But it requires a different attitude…less trust and more caution. The money rots faster than a ripe banana. Everyone struggles to get rid of it. People feel they have been ripped off — as they have — and then they don’t feel so bad about ripping other people off. A taxi driver may inflate his prices. A restaurant may give you the wrong change. A business may bill you incorrectly. And everyone will cheat on his taxes. Almost every major deal includes some ‘black’ money as well as some ‘white’ money. And then there’s the ‘blue’ money…the dollars you get from exchanging money at the free market rate; you don’t want to have too many of them, lest you have to explain where you got them. Every transaction requires quick calculations…and flexible book-keeping. Every relationship demands trust…and verification. And every experience comes with a certain amount of ambiguity…a moral and financial fluidity. It’s like having a picnic on the side of an active volcano; you need to relax in order to enjoy it… …but be ready to run. Regards,

Bill Bonner,

For The Daily Reckoning Australia Advertisement: How to Play Aussie Investors’ ‘Unfair Advantage’ We’re the world’s biggest lithium exporter. The third-biggest cobalt producer. And a major player in other critical minerals like nickel and rare earths. Australia is set to become a critical minerals powerhouse…and help the rest of the world recover from a supply crisis. I believe I’ve found the best way investors can capitalise on this ‘unfair advantage’. Click here to learn more. |

|

|