Today, we’re diving into one of the most fascinating corners of modern finance: pre-IPO shares.

Since startups are staying private longer than ever, there is huge demand to invest in high-quality companies before they go public.

You may recall our big issue last year on Destiny (NYSE:DXYZ), the first ETF for pre-IPO shares (whose own share price rapidly shot up and then sank)

This week I recorded a podcast with Christine Healey, the former Portfolio Manager at Destiny.

Christine shared some fascinating insights from her vast experience in pre-IPO markets, and how investors should navigate a world where companies are increasingly choosing to delay going public.

Christine Healey has a world of knowledge in this space. Along with her experience at Destiny, she was former Senior Director at Forge Global (NYSE:FRGE), and is now the founder of Healey Pre-IPO, a concierge broker service helping people invest in individual private tech stocks.

In Part 1 of the interview we explore:

The rise of structured products like the Destiny Tech100 Fund (NYSE:DXYZ)

Why DXYZ trades at a premium to its fundamental net asset value

How pre-IPO secondary markets differ from public markets

Essential factors that pre-IPO investors need to consider

How the pre-IPO market reacts to market volatility

In Part 2 we get into some juicy stuff:

Why Destiny’s model will be hard to replicate

The debate between closed-end vs interval fund structures

Her decision to go boutique and work hands-on with clients

Why accreditation is still an imperfect system

Exotic structures like layered SPVs and forward contracts

What the next 10 years of pre-IPO investing could look like

Launched in 2022, The Cashmere Fund lets anyone invest in pre-IPO startups — accredited or not.

Why invest in the Cashmere Fund

Open to everyone, not just the wealthy

Professionally managed portfolio of early-stage startups

Semiannual redemptions of up to 5% — not a 10-year lockup

Minimums start at just $500

And unlike Destiny’s DXYZ, which traded at a 1,000% premium just to access private companies, Cashmere offers a more stable, flexible approach — in an SEC-registered interval fund.

If you’re wondering how to get into private companies, this is a smart place to start.

To express interest in the Cashmere Fund without giving permission to email, click here.

Investors should carefully consider the investment objectives, risks, charges, and expenses of the Fund before investing. The prospectus contains this and other information about the Fund and can be obtained by calling 1-888-577-7987 or by visiting the Fund's website at thecashmerefund.com. All investments involve risks, and there is no guarantee that any portfolio company held by the Cashmere Fund will go public.

The rise of secondary markets

Pre-IPO shares are exactly what they sound like: equity in companies before they IPO.

Historically, this entire space was reserved for VCs, insiders, and well-connected accredited investors:

“It's been a trend for quite a few years now where companies that could go public...are choosing not to, or choosing to delay it sometimes five to ten years or longer. That means most investors miss the bulk of a company’s value creation. All that growth can only be captured by the investors that can invest while the company is private.” – Christine Healey

She's not exaggerating.

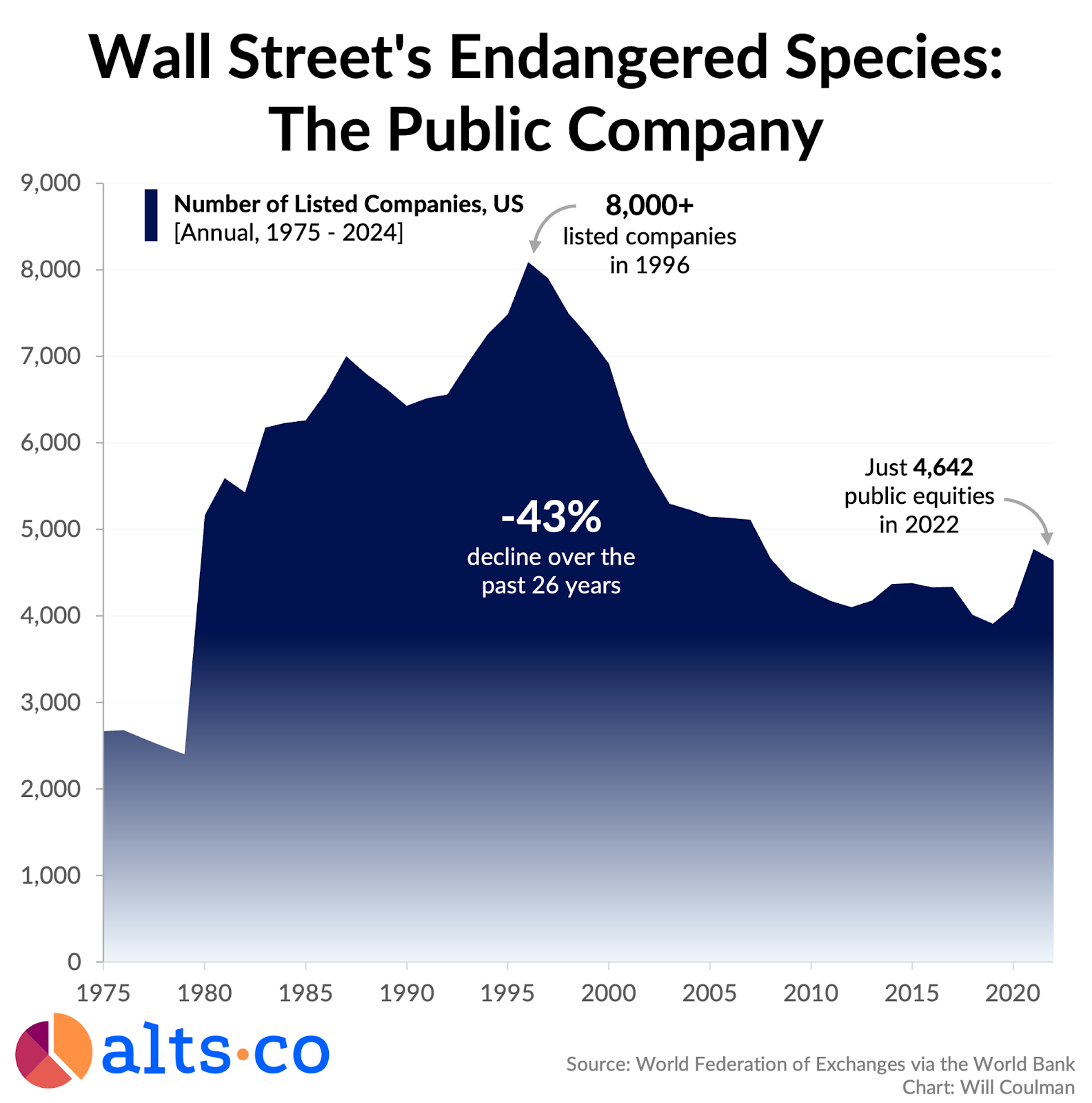

The need for secondary markets barely existed 30 years ago, because back then, companies went public far earlier.

But since the 1990s, the number of companies listed on US exchanges has dropped by 43% — and those that do IPO now often wait until they’re already worth billions.

Take Reddit, for example. The company took nearly two decades to go public. Stripe and SpaceX have been private for over a decade — and both are valued over $50 billion.

For retail investors, that’s a massive problem. By the time these companies finally reach the public markets, much of the explosive growth has already happened — captured by insiders, institutions, and early employees.

What’s left is often a slower, more mature phase of the business.

To put it another way: going public is no longer a starting line, it’s an exit.

“You used to be able to buy companies like Google early. Now you have companies like Reddit which were almost 20 years old when they IPO'd SpaceX [is] modeling this idea of staying private for a really long time, keeping tight control over the company, tight control of shares, and staying laser focused on a mission.” - Christine Healey

Shares in these startups are now trickling out to a broader audience — albeit slowly — through funds like Cashmere.

But we still have a long way to go.

“There are PhDs in rocket science who can’t invest in SpaceX because they're not accredited. It’s a broken system.” - Christine Healey

We spoke a lot about where private share investing might be headed in the future. (Kaylock was an early employee at EquityZen, so this is a space he knows well.)

One thing we discussed was how odd the current regulations are for private share investing:

Regulators like the SEC treat buying private shares as far riskier than buying public shares. (And sure, that makes sense, since there’s less disclosure.)

But the result of tighter regulation is less access: it’s harder for companies to sell shares, harder for investors to buy them, and harder for financial intermediaries to connect the two.

And at the same time, regulators are happy to let investors easily buy a range of risky assets like levered ETFs, zero-day options, and, well, crypto.

This seems very inconsistent to me!

Are private shares really that much riskier than what investors can already buy on their brokerage app? Why is ‘disclosure risk’ treated so uniquely?

On the supply side, something from my conversation with Christine stuck with me: The idea that offering liquidity for equity compensation is a big hiring advantage for private startups.

Right now there is a natural tension between private companies wanting greater control over their shareholders, and employees (who are also shareholders) wanting greater access and liquidity.

The difficult reality is that many early employees at successful startups have money "on paper" that they can't access because it's locked up in illiquid shares.

This dynamic also affects where top talent chooses to work.

"If you're an AI engineer right now and one company has very liquid access to the shares that they're compensating you with, and the other doesn't, that's going to have a real impact right on the company that you want to work for" - Brian Flaherty

Christine agreed:

"To succeed and attract the best talent, they will need to empower their employees and investors with greater liquidity."

The good news is that models for this already exist. Stripe frequently conducts tender offers for their own shares to provide employee liquidity.

But this strikes me as one of the strongest structural reasons that a private company would want to foster a market for their shares, even if they don’t need to raise capital.

I don’t know exactly what the future holds for private share investing – but between demand- and supply-side factors, the time has never looked better for new market models to emerge.

Watch Part 2 of our interview

Join Altea to watch Part 2 of my interview with Christine.

Altea Gateway (formerly known as the All-Access Pass) is your ticket to Altea. It unlocks all investments, content, perks, and private spaces within the community.

It's perfect for investors who want essential access to Altea.

What you get:

Remove all paywalls (like this)

Get access to all Altea SPVs

2% management fee, 20% carried interest on SPVs

Access to all private community spaces

Access to member perks and partner discounts

Join one free local meetup per year

I don't mean to pat ourselves on the back, but joining Altea can pay for itself 10x over.

This quote from Altea Member John Nikolaou says it all:

"Thanks again for your original Destiny feature! I invested and it paid for my entire Spain trip, as it went public at $9/share, then cruised to the mid $90s. That's the kind of tax problem I like to have! - John Nikolaou