| | By Greg Canavan | | Editor, Fat Tail Daily |

|

| In this issue: - What’s Not Priced In — A knee-jerk rally, don’t get excited

- The breakdown of the renewable energy boom

- Bill Bonner: Political rifts, tech battles, trade tariffs and currency wars...

|

|

[1 min read]

Dear Reader,

$32.8 billion worth of cost blowouts on an $80 billion infrastructure program?

That’s 40% inflation.

How much of it is actual inflation versus planning incompetence is another question. But it does tell you how bad the government and bureaucrats are at economic management.

I mean, they’re running a huge population boom. This puts massive pressure on a nation’s infrastructure. You’re seeing this most acutely in the housing market.

But we can’t simply build more housing to keep up. Developers who own the land slowly release new supply to ensure strong prices. High inflation and interest rates make it tough for builders.

And we’re diverting huge resources into an energy transition that will deliver higher energy prices down the track!

Brilliant!

Meanwhile, the stock market rally looks like pausing here. As I point out in the latest What’s Not Priced In episode below, stock markets in the US and here are now ‘overbought’. They’re due for a correction.

The recent rally is all about relief that we’ve seen a peak in inflation. That may be so in the US. But with the current economic mismanagement, Australia may find the inflation fight tougher.

And that means an RBA that will keep rates at elevated levels for some time.

Against this backdrop, it’s hard to see how the rally continues…  | | By Kiryll Prakapenka | | Editor, Fat Tail Daily |

|

[4 min read] Dear Reader, Champagne or water? Excess or temperance? That’s the question posed this week. 10 basis points. That’s all it took. US inflation came in 10 basis points lower than expected on Wednesday. Stocks surged. Champagne flowed. Following the US CPI release, US 10-Year bond yields fell nearly 20 basis points. The biggest one-day fall since the collapse of Silicon Valley Bank. But a 0.1% inflation ‘beat’ is not comparable to the genuine fright caused by SVB’s collapse. There’s a technical term for Wednesday’s rally. Kneejerk reaction. The champagne didn’t flow for long. The rally, much like the drink, lost its fizz. Since Wednesday, the S&P 500 is flat. Aussie stocks are down. Wednesday’s jubilance is today’s hangover. In markets, temperance is cool. As for the latest episode of What’s Not Priced In, Greg and I discuss: - Whether or not the US inflation data was significant

- Australia’s historic wages growth and what it means for interest rates

- Valuations of the Big Four banks

- They look cheap, but there’s more to it

- Outlook for cashed up Aussie gold miners

- Unappreciated insights from the RBA’s latest Statement

- High mortgage repayments don’t tell the whole story

- Accumulated savings offsetting RBA’s rate hikes

RBA’s ‘last mile’ will be a slog

I want to talk about the Reserve Bank’s inflation challenge.

In my view, taming inflation will be harder than markets think.

Inflation’s ‘last mile’ will be a slog. For a few reasons.

One of them is wages growth.

This week, the ABS released the latest Wage Price Index data.

The WPI rose 1.3% in the September quarter and 4% for the year. The ABS said it was the highest quarterly growth in the 26-year history of the WPI.

The annual growth was the highest since March, 2009.

The data didn’t faze the market upon release. But I wonder if it’ll phase the RBA.

Services inflation is the bank’s bugbear. It’s stickier than officials predicted.

And rising wages play a big role in that stickiness.

Now, high wages growth is fine if productivity is high, too. But Australia’s productivity is poor.

In the latest Statement, the RBA said:

‘Even so, the cost of labour for firms also depends on growth in labour productivity, which has been very weak. As a result, growth in the cost of labour is very high and is adding to firms’ overall cost pressures; the forecasts assume that productivity growth will pick up, which will be needed for labour cost growth to be consistent with the inflation target.’

But what if productivity doesn’t pick up? The RBA’s forecasts were wrong before.

I think wages growth remaining high is more likely than productivity suddenly improving. Even the RBA expects wages growth to decline slower than overall inflation.

Mortgage repayments rising, but overall debt servicing low

Another challenge for the RBA is mortgage repayments.

But not for the obvious reasons.

Mortgage repayments are at record highs relative to disposable income. That dents aggregate demand.

Maybe not as much as the RBA would like.

In the latest Statement on Monetary Policy, the RBA said scheduled mortgage payments rose to ~10% of household disposable income in the September quarter.

But…

The RBA also noted Australia’s stock of personal debt fell ‘substantially’ in the last 15 years.

The overall debt servicing burden for households ‘appears to be lower than in 2008’.

Interesting.

And who knows, maybe households are more comfortable with higher mortgage repayments because their other debt burdens are at multi-decade lows.

Population growth

Another challenge is population growth. Or, population growth outpacing supply.

I’m seeing more editorials in the financial press worrying about this.

Future Fund chairman Peter Costello was one such worrywart.

Costello said this week:

‘Australia has always been a migrant country, and I’ve always supported immigration. But the levels of immigration now are extremely high.’

Population growth is certainly straining housing supply. Rents are rising. So, too, are house prices.

The supply of housing is less flexible than ‘supply’ of people.

But the Reserve Bank is less concerned.

In the Statement, the RBA pointed out that more people equals more demand and more supply:

‘Population growth has been substantially stronger than expected following the reopening of the border. However, the net effects on the aggregate inflation outlook and the unemployment rate have been relatively small… The increase in population has added to both aggregate supply and aggregate demand in the economy.’

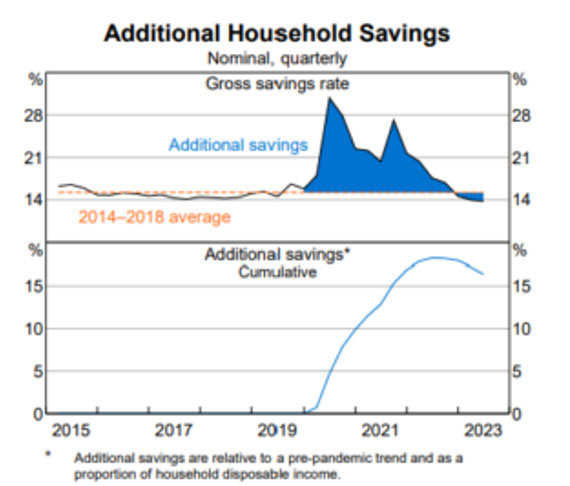

Accumulated household savings

Yet another challenge for the RBA is our savings.

Inflation’s intransigence stumped many.

But the chart below may explain why.

We accumulated enormous savings during the pandemic.

For many, these additional savings — savings above what you’d expect prior to the pandemic — still remain.

Fat tail risk: unanchored inflation expectations Where do you think inflation will be in 2024 and 2025? Our opinions about future inflation matter. And the Reserve Bank knows they matter. Our inflation predictions influence the present. Anticipating inflation tomorrow, we bring about inflation today. That’s why managing expectations is a big part of the RBA’s job description. So here’s the RBA’s final challenge. A fat tail risk. Unlikely, but worth considering… Inflation expectations unmooring. The RBA described this scenario a while back: ‘But if the inflation psychology of households and firms shifts and inflation expectations move away from the central bank's inflation target (i.e. they become ‘unanchored’), a period of higher inflation will become persistent because households and firms will expect inflation to be higher in the future and adjust their behaviour accordingly. Consequently, it is much easier for a central bank to manage inflation if inflation expectations are anchored rather than unanchored.’ If markets want rates to fall, they better wish our inflation expectations remain anchored. Yet the risk of expectations unanchoring, while not worrisome now, is rising. And it will keep rising with each missed inflation forecast by the RBA. The latest Statement was riddled with admissions inflation continues to surprise Bank officials. This Monday, RBA’s acting assistant governor Marion Kohler made another. The next stage in bringing inflation down to the RBA’s target is ‘likely to be more drawn out than the first’. The ‘road ahead could be bumpy’. And of the ‘key risks’ Kohler identified was inflation expectations untethering. Kohler said: ‘One of the key risks is the possibility that high inflation today could lead households and businesses to expect high inflation in the future, putting upwards pressure on actual prices and wages. Encouragingly, measures of medium-term inflation expectations have generally remained consistent with the Bank’s inflation target. But, if high inflation did become entrenched in people’s expectations, it would be very costly to unwind, involving even higher interest rates and a larger rise in unemployment. Here’s a fat tail risk to watch!

Regards,

Kiryll Prakapenka,

Editor, Fat Tail Daily Advertisement: The Hidden Dangers Of Buying Dividend Stocks

Getting a fat dividend payment is great… But if you’re not careful, you may find your nest egg shrinking faster than you planned — because the company paying that dividend is losing market value. That’s the last thing you want if you’re relying on dividends for income, especially if you don’t have time on your side to make up any shortfalls. But what if you could have a stable income AND see your capital steadily increase over time? Imagine the peace of mind that could bring. Well, Greg Canavan believes he’s found six ASX-listed stocks that can do exactly that. Click here to learn more. |

|

| The Wind Industry Proves as Intermittent as its Power |

| | By Nick Hubble | | Editor, Fat Tail Daily |

|

[5 min read] Dear Reader, What if renewable energy is just a figment of free money? Or should I say ‘was’? Zero percent interest rates set a remarkably low financing bar for a wind project to leap over on paper. And it’s not like wind developers struggled to access favourable terms from governments when it came to selling their intermittent power either. But then interest rates rose and inflation struck. The cold hard economic truth is exposed… Like a rock star who got his money for nothing and his wind for free, the wind industry went too far and then keeled over on stage. The Global X Wind Energy ETF [NASDAQ:WNDY] has halved in two years amidst what’s supposed to be a planet-saving buildout. The Austrian School of Economics, which bears that name as an insult from the German School, has a theory which explains what happened. They imaginatively call it The Austrian Business Cycle Theory and ‘malinvestment’. In short, when central banks suppress interest rates artificially by inflating the money supply, this causes more capital investments to occur. Debt is made artificially cheap, encouraging debt-intensive projects to go ahead. Wind energy being an obvious example of this, because the wind and sun may be free, but turbines and solar panels are definitely not. Unlike for fossil fuels, which require constant purchases of more fuel — spreading out the cost of energy over time — renewables face a vast upfront cost to be built, and low marginal costs after that…presuming they are built properly…which many weren’t. But back to our Austrian story. The low interest rates make such capital investment seem profitable because the costs of borrowing to finance them are low. This was especially potent for wind farm developers because of the minimum power prices they were often promised under supply deals. But, because the capital investment boom is financed by dodgy money from central banks, it eventually causes inflation. By the time wind farm developers were ready to build, their costs had soared as fast as Australian builders’. This contrasts starkly with what would happen under the same sort of scenario under sound money. In such a system, interest rates can only fall due to more savings, not more money printing. And more savings mean higher future consumption. That higher future consumption is what justifies the capital investment which the savings financed in the first place. The whole thing balances out, with investments occurring in anticipation of producing something that consumers will be able to afford to buy. But artificial money causes inflation to show up instead of higher future consumption. And that inflation is what’s bringing down the wind industry. Ironically, of course, the medicine for inflation is higher interest rates — the one thing which wind developers cannot afford when their costs are going up. It becomes a double whammy. And so the artificial boom turns to an overzealous bust… In the UK, the Telegraph is on the case: ‘The UK’s leading offshore wind developer is in talks with Net Zero Secretary Claire Coutinho about the fate of its flagship project off the coast of Norfolk, after spiralling costs cast doubt over its viability. ‘Ørsted, the Danish renewable energy giant, is understood to be in talks with the Department for Energy Security and Net Zero, led by Ms Coutinho, about securing more generous subsidy arrangements for its Hornsea 3 wind farm project. ‘It would see 231 turbines installed off the coasts of Norfolk and Lincolnshire, generating power for 3m homes. ‘Subsidies for Hornsea 3 were agreed with the Government last year through contracts for difference (CfDs), with operators guaranteed a minimum price per megawatt hour (MWh) known as the strike price. Ørsted was promised £37.35. ‘However, the wind industry has been hammered by inflation of up to 40pc since then. Building Hornsea 3 would now put Ørsted at risk of significant losses and executives warned earlier this year that they needed more government support to keep the project alive.’ The Financial Times reported on the US: ‘This week Ørsted, the world’s largest offshore wind energy developer, abandoned two projects designed to deliver 2.2 gigawatts of power to New Jersey. BP’s head of low-carbon energy, Anja-Isabel Dotzenrath, told a Financial Times conference that the US offshore wind sector was “fundamentally broken”.’ Yahoo Finance revealed the fate of Siemens Energy: ‘The German government, Siemens AG, and other parties will provide billions of euros in project-related guarantees to support Siemens AG's struggling wind turbine division. This financial assistance comes just weeks after the company warned about mounting losses amid a meltdown across wind and solar industries.’ Bloomberg covered events in Norway: ‘Orsted A/S has withdrawn from a partnership developing offshore wind projects in Norway as the company grapples with big losses resulting from rising costs. ‘Orsted is at the center of a crisis for the offshore wind industry with companies struggling to fund large developments. Higher financing and component costs combined with increased competition have slowed the pace of renewable energy around the world, making it harder for developers and suppliers to make new projects profitable.’ These comments from the UK’s Telegraph sum up the situation: ‘No new wind farms will be built off Britain’s shores unless the Government lets operators earn more money from the electricity they produce, the chief of the nation’s biggest generator has said. ‘Tom Glover, country chair of RWE’s UK arm, said the price offered by the Government to wind farm operators must rise by as much as 70pc to entice companies to build. ‘His warning follows the disastrous result of the last offshore wind allocation round in September, which ended in a humiliation for ministers with not one company offering to build new offshore wind farms.’ All this is a remarkable turnaround for an industry that is accustomed to getting paid hundreds of millions to produce nothing. Or getting paid a minimum price to produce energy even when the wholesale power price goes negative because the energy isn’t needed. Talk about misaligned incentives… It’s important to remember that both the inflation and the higher interest rate environment that is sinking the wind industry are a direct cause of the artificial boom which caused it to expand so much in the first place. The bust is the market correcting the malinvestment that occurred on the back of the artificial stimulus. It undoes the projects that shouldn’t have been built in the first place. This contrasts starkly with modern economics’ theories, which include the ‘neutrality of money’ — the idea that inflation doesn’t really matter much because it impacts us all evenly and inflation expectations just mean we all adjust anyway. Only modern economists seem to have forgotten to send that memo to wind farm developers alongside central bankers, neither of whom were ready for the inflation we got. The real worry is whether this now becomes some sort of self-reinforcing cycle. I mean the cost of energy plays a rather important role in inflation figures and thereby interest rates in and of itself. If wind farm developers need vastly higher prices, the rest of us are going to pay for them. And that means more inflation. But it may not come to that. We may get the inflation via an energy shortage instead… Orsted is so desperate to evade building the wind farms it committed to that it’s willing to take on impairment charges measured in the billions of dollars instead. Equinor and BP joined in, with combined impairment charges on wind projects hitting $5 billion in a single week. Renewables are looking so expensive that even major oil companies can’t afford them as a form of virtue signalling anymore. One after another, they’re scaling down their green plans. That’s what happens when you have to finance yourself with positive interest rates. Suddenly money matters. There’s even a rumour that BP will change its name from ‘Beyond Petroleum’ to ‘Back to Petroleum’…although I admit I am the only source of the rumour… The real point here is that the renewables sector is conforming rather nicely to the same economic theory that explained the US housing bubble and bust of 2008, and many other crises since. An artificially inflated bubble blown by low interest rates and directed by government incentives eventually pops in a crisis of inflation and higher interest rates. That’s just what you get when central bankers keep fiddling with the interest rate and the money supply. So, don’t blame the renewables sector, blame the central bank for tricking them into thinking their business was viable in the first place. Until next time,

Nick Hubble,

Editor, Fat Tail Daily Advertisement: Is ‘Hyper-bitcoinisation’ Inevitable? Ryan Dinse’s Oct 2022 video mapped out Bitcoin reaching US$1 million.

Crypto winter has ended precisely on schedule…now see the rest of this bold prediction.

Rewatch how the timeline goes from here. |

|

Friday, 17 November 2023  | | By Bill Bonner | | Editor, Fat Tail Daily |

|

[4 min read] Dear Reader, Let’s turn to the money itself. There’s more to the story there, too. The ‘West’ may be failing politically…maybe even technologically…but when it comes to making money, nobody does it better, right? The stock market is booming. Unemployment is low. As for ‘inflate or die’…our hypothesis, that a system that thrives on more and more credit must continue ‘inflating’ or it will collapse…maybe we are wrong? Maybe inflation will come down with no need to pop the bubble? First, the latest news, MarketsInsider: Bonds go bonkers as the US government now pays more than Vietnam or Morocco to borrow …the US is the world's biggest economy, with the biggest businesses, and is a magnet for global investors. Such unrivaled economic muscle would mean the American government can borrow money much more cheaply than other sovereign entities — especially, emerging-market nations with weaker credit ratings. Today, the world’s strongest borrower — the US government — pays more for its loans than some of the world’s weakest borrowers. The US borrows money at 4.5% (the 10-year T-bond)…while Vietnam pays only 2.8%. This is just one of many contradictions and puzzles that bedevil the whole ‘western’ world. Nothing is quite what it pretends to be...or used to be. Chimerica But the ‘more to the story’ is that the US government has an almost unbroken chain of deficits going back to the Carter administration. The national debt now totals $33.5 trillion…and it’s still growing fast. America’s trade deficits, too, began in the 1970s…and haven’t let up since. It now owes the rest of the world $18 trillion in accumulated deficits (currently running at about $1 trillion/year.). More to the story there, too. China invested way too much money (much of it borrowed) in order to develop output capacity for people who really couldn’t afford it. And as they put more and more peasants to work, fewer were left to be absorbed into their factories. It became harder and harder to keep wages (and prices) low. And then, too, when the US revealed that it was not above ‘sanctioning’ foreign nations and seizing their assets, the ‘world’s most successful joint venture,’ began to fall apart. The New York Times is on the case: Americans treated China like the mother of all outlet stores, purchasing staggering quantities of low-priced factory goods. Major brands exploited China as the ultimate means of cutting costs, manufacturing their products in a land where wages are low and unions are banned. As Chinese industry filled American homes with electronics and furniture, factory jobs lifted hundreds of millions of Chinese from poverty. China’s leaders used the proceeds of the export juggernaut to buy trillions of dollars of US government bonds, keeping America’s borrowing costs low and allowing its spending bonanza to continue. Chimerica has yielded to a trade war, with both sides extending steep tariffs and curbs on critical exports — from advanced technology to minerals used to make electric vehicles. Deficits, Debts…and Disaster It was nice while it lasted. Now, the foreigners are no longer holding down prices for US consumers. So, the Fed had to stop buying bonds, and raise interest rates, in order to bring inflation down to its 2% target. The Chinese aren’t buying bonds either. Axios: - In China, the economy — and the currency — are weakening. It now may even be selling some of its Treasuries as it tries to support its slumping currency.

- Further, the worsening relationship between the US and China — as well as America's sanctions on Russia after its invasion of Ukraine — might be giving Beijing a reason to reduce its exposure to the US financial system.

The US still borrows huge amounts of money. The average interest rate on consumer credit card purchases is now over 21%. Bloomberg reports that some auto buyers are paying 29% on their car loans. Mortgage rates have come down, but are still twice what they were three years ago. Meanwhile, the largest borrower in the world — the US federal government — runs a deficit of $7 billion every day, Monday through Friday. And it has some $7.6 trillion in old loans that it must roll over in the next 12 months. Its two major lenders — China and the Fed — have both stopped buying. Shouldn’t the feds cut back…and stop borrowing so much money? Improv Policy But instead of even addressing the subject, Congress is doing a kind of ‘improv’ fiscal policy…making it up as it goes along. No budget. No balance. No long-term plan. And no hope of getting excess spending under control. Business Insider has the latest: Congress just found the dumbest way to avoid a shutdown Under a plan backed by House Speaker Mike Johnson, the federal government would be funded through the new year. After that, different agencies would face different deadlines for potential partial government shutdowns. For example, funding for the Pentagon and veterans would run out on January 19. Funds for the State, Justice, and Health and Human Services department would be extended until February 2. "That's the craziest, stupidest thing I've ever heard of," [says] Democratic Sen. Patty Murray. “You'd have to go through the threat of shutdowns of part of [the] government over and over again," [senator Susan] Collins said. Under the circumstances, the wonder is not that US borrowing costs are so high…but that they are not higher. But it’s probably just a matter of time…before the real cost of borrowing goes up more. Stay tuned… Regards,

Bill Bonner,

For Fat Tail Daily All advice is general advice and has not taken into account your personal circumstances. Please seek independent financial advice regarding your own situation, or if in doubt about the suitability of an investment. |

|

Advertisement: Australia’s ‘Big Squeeze’ Imminent? In the past, setups like this have sent certain Aussie resource stocks flying. Could history soon repeat itself? Full story here. |

|

|