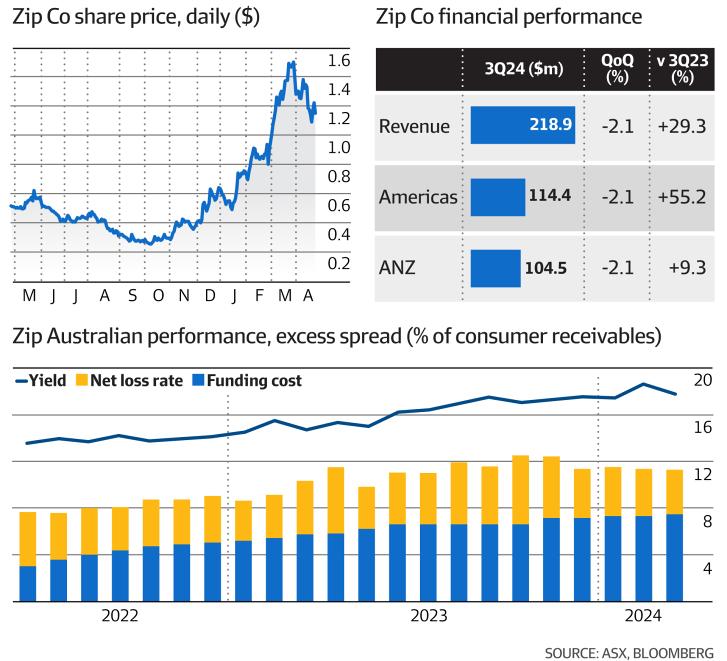

A mid-April market update shows Zip, which has bet heavily on the lucrative US market, is tracking ahead of expectations. The company reported $20.1 million cash EBITDA in the third quarter of 2024 thanks to a strong performance from its US division (see chart below) and upgraded its second-half guidance. Its US growth is also on track, revenue up 50 per cent year-on-year and transaction volume jumping 44 per cent. |